Pre-writing, Argumentative Essay Introduction and

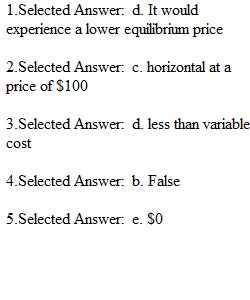

Q 1.Suppose a perfectly competitive increasing-cost industry is in long-run equilibrium when market demand suddenly decreases. What might happen to the typical firm in the long run?2.Question 2 10 out of 10 points Exhibit 8-1 Demand Cost Price Q Q Marginal cost $60 5 1 $50 80 4 2 60 100 3 3 100 120 2 4 140 The perfectly competitive firewood market is composed of 1,000 identical consumers and 1,000 identical firms. Exhibit 8-1 shows cost data for one firm and demand data for one consumer. What does the demand curve facing a single firm look like? 3.In the short run, a perfectly competitive firm will always shut down if, at all positive output levels, total revenue is4. In perfect competition, each firm's output is a large fraction of total market supply. 5. In the short run, if a firm shuts down, its total revenue is

View Related Questions